Article | May 13, 2021

What types of brands compete in the fresh coffee market?

The pandemic reveals the advantages and disadvantages depending on the type of brand. In addition, the proximity and image perceived by the consumer were key to their sales.

.jpeg)

The brand is a valuable intangible asset for the differentiation of a company, as it has a unique symbolism that leads a consumer to repeatedly search for it. Of course, this behavior will vary by product category and country. However, when it comes to coffee, brand preference and local production tend to be clearly aligned. For example, this product has become synonymous with Colombia. The same is true when consumers perceive their country's specialization in a product category, such as tea in Vietnam and chocolate in Belgium and Switzerland.

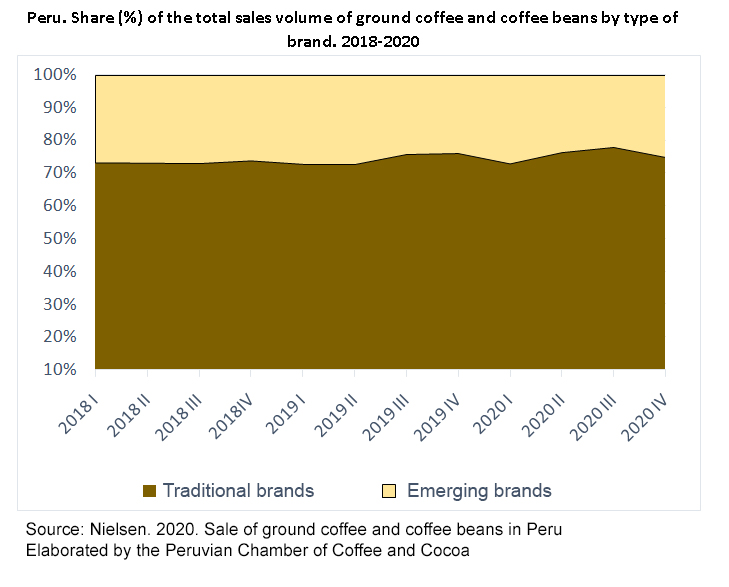

For the fresh coffee category in the Peruvian market, the consumer relojes replicas has the expectation that the brand he chooses must have the best taste that he can find and pay for. The brands with the longest time selling ground coffee and beans are the ones that have managed to consolidate their image until they are recognized as traditional brands. Time has even allowed them to strengthen their distribution infrastructure to be on the shelf of the nearest winery, market or supermarket.

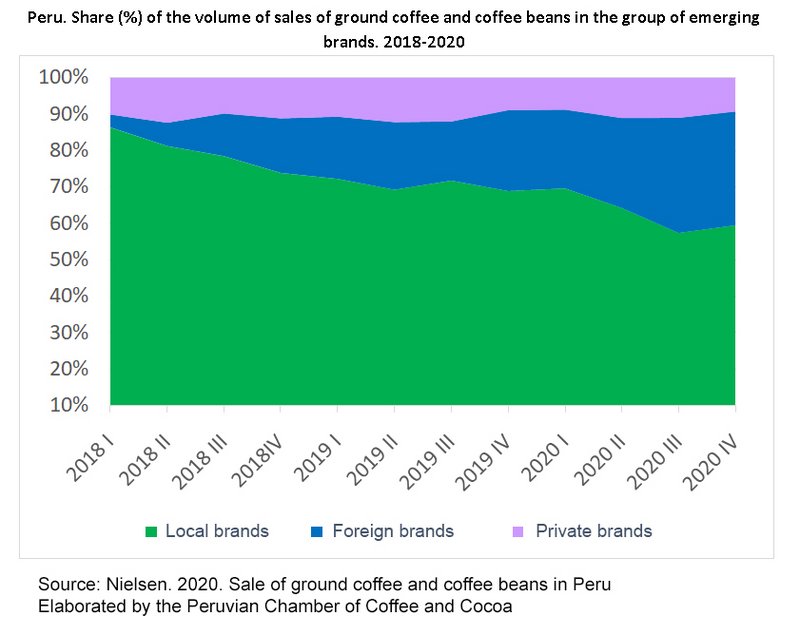

On the other hand, there is a group of fresh coffee brands that have been making their way in recent years, and even being in a training stage in terms of positioning, they maintain their coverage in the retail channel of sale to the public, also showing resilience during the pandemic. We have called this second group of brands emerging and it includes private, local and foreign brands.

The difference in sales capacity in both groups of brands was evident during the pandemic. While in the 2019-20 period, traditional brands increased their sales volume by 5%, that of emerging brands decreased by 1%. Given the economic and health insecurity perceived by consumers, they opted for the first group as it projects confidence and availability in the points of sale closest to the home.

The sale of fresh coffee loses its seasonality

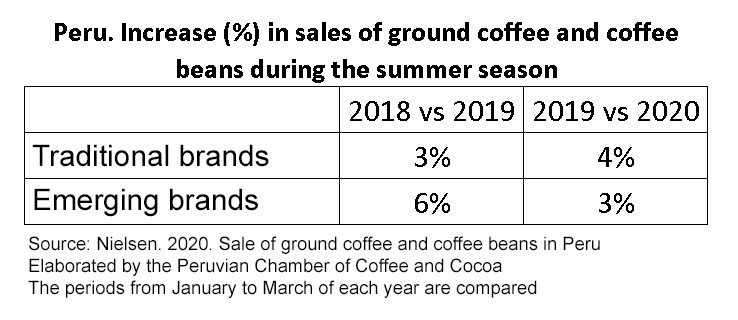

It is important to note that in the last two years the sale of fresh coffee has increased in the summer season. Despite the fluctuations that are perceived at first glance, if you pay attention to the volume of sales of each group of brands in the market during the first quarter of each year, you will see an increase compared to the previous one.

It is well known that traditional brands are the ones that most promote the sale of fresh and ground coffee regardless of the season of the year. The promotion of the mass consumption of this product, in addition to the premiumization, highlights its strategy of adaptation to the value proposition of taste and quality at a fair price that most Peruvian households seek in the COVID-19 context.

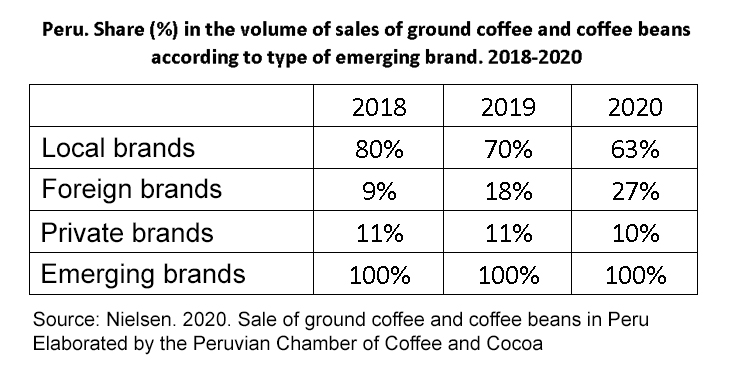

Emerging brands

In emerging brands we find three groups: local, foreign and white. Local brands lead the group, some are national in scope with several years and seeking to consolidate their position in the market, but we also find a growing group of regional brands that advance and may even lead specific places, where their preference is broad. These local brands have sustained a participation of more than 50% of the sub-category in the last two years, although after the pandemic it was reduced by 7%, the recognition of these brands would not be the problem, but rather their availability on the shelf.

Local brands have greater coverage in the main points of sale in the country such as wineries and markets. However, the pandemic has affected the logistics chain of its suppliers to supply these channels. The effect is visible in the drop in sales volume since the first quarters of 2020, closing the year with a decrease of 12%.

Stores and markets: favorite places to buy local coffee

In the country there is a strong emotional value associated with the shopping experience in the traditional retail channel. Studies have shown that this is a critical determinant of consumer loyalty. For this reason, wineries and markets use their physical and human resources to create a pleasant atmosphere in the store that allows the consumer to feel good and enjoy their purchases.

Flexibility is the key strength of these points of sale, since the assortment of products they offer can vary and it is the same vendors who make the decisions. However, its poorly standardized operating processes can jeopardize the continuous experience provided to the consumer in the fresh produce categories. As it happened during the pandemic, when consumers looking for fresh local coffee found it less frequently. Then, other brands were allowed to remain accessible during this period.

In this sense, despite the fact that foreign brands have a participation of the total volume of sales in the group of less than 30%, this increased considerably. The pandemic revealed its advantage, and by preventing global companies, operations for its commercialization are more efficient and predictable. This helped to counteract the impact on the logistics chain and to offer their fresh coffee in supermarkets, getting closer to the final consumer.

Fresh coffee is also sold under private labels, which are brands belonging to a hyper or supermarkets distribution chain and which have the objective of achieving commercial loyalty for the articles of the establishment.

Private brands of ground coffee and beans have a share of less than or equal to 11%. Its sales volume fell by 10% during the pandemic. The Peruvian consumer tends to prefer white brands when it comes to products considered basic due to their low prices, and they come to know them through the advertising displayed by the supermarkets where they are sold.

During the pandemic, consumers were restricted to the level of non-essential expenses. For this reason, they were more willing to choose slightly more expensive, but better tasting, brands for the foods and beverages in their basic basket. In this way, they seek at least to indulge themselves with "something special."

Based on the above, we can affirm that currently more fresh coffee is bought, with ground coffee and beans being a small consent to enjoy at home. The brands of fresh coffee that can retain or increase consumers seeking this product will be those whose manufacturers can supply them without interruption to reinforce their position in the minds of consumers and motivate their repeat purchases.

It is important to note that sales in new channels, particularly online, and the progressive expansion of coffee shops as points of sale, are a phenomenon that complements this view. We will be addressing this topic in our next informational articles.

How does the dynamics of the brands differ in the cities of the country? Currently, the Peruvian Chamber of Coffee and Cacao is working on an upcoming publication to answer this question. This effort is carried out within the framework of the Alliance for Sustainable and Competitive Coffee Project, in which the National Coffee Board also participates as executor and receives the support of the SeCompetitive Program of the Swiss Cooperation SECO, in collaboration with Helvetas Peru and the Embassy Switzerland in the country. Each note is an important input, "a drop that adds" to the development of the National Plan for the Promotion of Coffee Consumption.

SeCompetitivo Program Facebook: https://www.facebook.com/SeCompetitivo/

Facebook of the Peruvian Chamber of Coffee and Cacao: https://www.facebook.com/camcafeperu

________________________________________________________________________________________________

References:

- The Nielsen Company. 2020. Sales volume of ground and bean coffee in Peru.- Database acquired by the Sustainable and Competitive Coffee Alliance Project

- The Nielsen Company 2018. How to Prepare for a Brand Coverage Analysis.

- The Nielsen Company. 2016. Done where?. Perceptions about the origin of brands delineate purchasing intentions around the world.

- ACEI. 2020. [Colombian Association of Market Research and Public Opinion Companies]. Nielsen: Life Beyond COVID-19.

- Caluda Inga Martínez (March 30, 2020). Coronavirus generates drastic changes, what are they and how long will they last? El Comercio.

- Retail news (July 31, 2020). Covid-19. 53% of Peruvians buy in markets and stores. Peru Retail.

- Retail news (January 28, 2020). What is a private label and why do Peruvians prefer it? Peru Retail

- Castro, L. 2019. The influence of the brand experience in the positioning, loyalty and brand value in the coffee shops of the city of Manizales.

- Ruiz, E. 2009. Perceived value, attitude and customer loyalty in retail. 2009. Universia Business Review, (21): 102-117.