Article | Nov 03, 2021

Resisting the crisis: the performance of coffee and cocoa growers in a pandemic

As the country recovers from the recession, producers have benefited from a favorable environment and are diversifying their income.

.jpg)

2020 left a negative balance not only in terms of health, but also in the economy of millions of families in our country. Between 2019 and 2020 there was a notable increase in total poverty (+9.9%), urban (+11.4%) and rural (+4.9%), and a significant increase in informality (+4.6%). Figures that meant a setback of 10, 13, 6 and 11 years, respectively.

Despite this, the agricultural sector remained active, since a large part of our country's food security and an important part of international trade through its agro-export products depend on it. In this sense, how did the coffee and cocoa producers fare? How did the situation affect them? and how did they respond?

Incidence of poverty

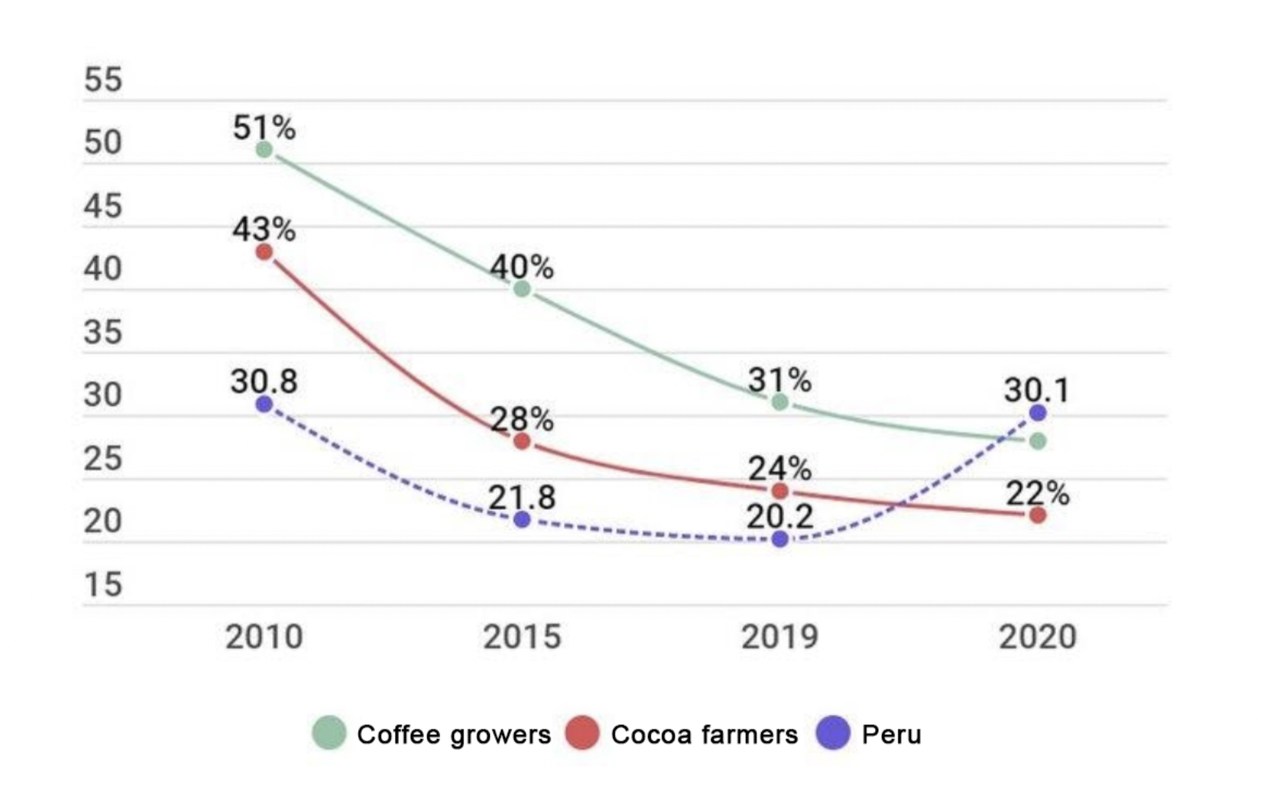

Contrary to the national trend, the incidence of poverty in the coffee and cocoa sectors was reduced. Between 2019 and 2020, more than 8,000 coffee growers and 48,000 cocoa growers ceased to be poor in the country, which meant reductions of 3% and 3.5% in poverty rates, respectively.

When considering the situation of the last ten years (see graph 1), it can be confirmed that the socioeconomic dynamics of coffee and cocoa growing families has remained stable despite the ravages caused by the pandemic.

Graph 1. Evolution of national poverty and in producers

Source: National Household Survey (ENAHO), various years.

Although poverty has not increased in both sectors, this does not indicate that the economic situation has not been difficult, since for the identification of poverty the different items of income are taken into account (approximated by the expenditure method), including those from State transfers, remittances and other extraordinary income, which is why their real status may be attenuated by these non-labour sources.

Sales and income strategies

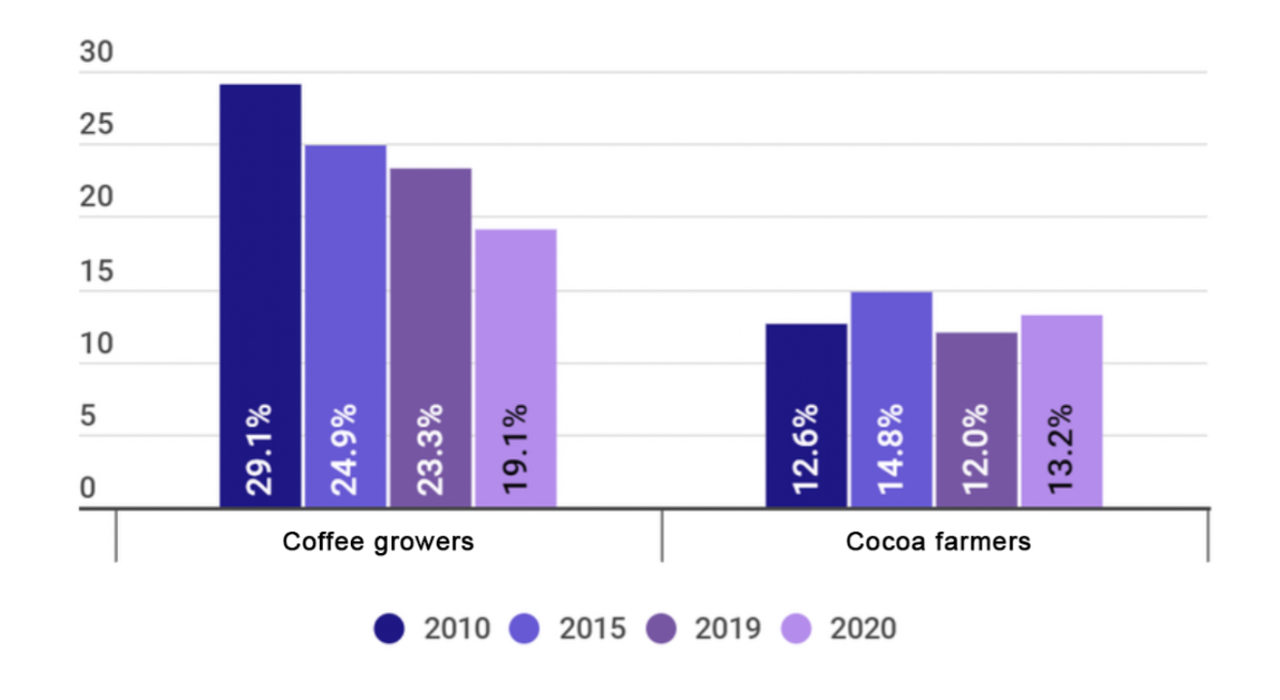

One way to track the underlying impacts of the pandemic in both cases is through a look at the sector's own revenues. The most useful indicator is the weight of income from the sale of coffee or cocoa within total household income (see Figure 2).

Graph 2. Share of coffee and cocoa sales in total household income

Source: National Household Survey (ENAHO), various years.

Analysis of coffee activity

For coffee, income had an adverse impact, since the weight of coffee sales over total income had a greater variation in the 2019-2020 period compared to the 2015-2019 period. In other words, the coffee activity, in the context of the pandemic, had a significant drop within the composition of family income.

The above has two implications. On the one hand, it would mean that annual income from coffee sales fell (the survey indicates that they went from 3.5 thousand soles in 2019 to 3.4 thousand soles in 2020, on average) and, on the other hand, that the other sources of income acquired greater prominence (the survey supports that income from other sources went from 11.6 thousand soles to 14.5 thousand soles, on average). The latter means that coffee families probably adopted income diversification strategies such as new crops or employing themselves in other activities to stabilize their economies.

Analysis of cocoa activity

In the case of cocoa, the weight of income from cocoa sales in total income increased between 2019 and 2020, going from 12% to 13.2%. This change may be due either to a nominal increase in cocoa sales in excess of other sources of income, or to a reduction in other income.

The review of the survey corroborates that income from cocoa sales hardly moved between 2019 and 2020, so the change in the importance of cocoa in total income is due to a reduction in other sources of income. The foregoing makes it clear that state transfers could not offset the reduction in other sources of income for cocoa farmers.

Source: Pixabay

Beyond the difficulties, it is important to point out that both coffee and cocoa producers had a positive performance, which was reflected in the reductions in the incidence of poverty despite the health crisis. It would be worth noting that, despite the logistical complications caused by the pandemic (difficulties in collection, shipping, etc.), external conditions were favorable for domestic production; and the countryside has responded by maintaining its production levels.

Price effects

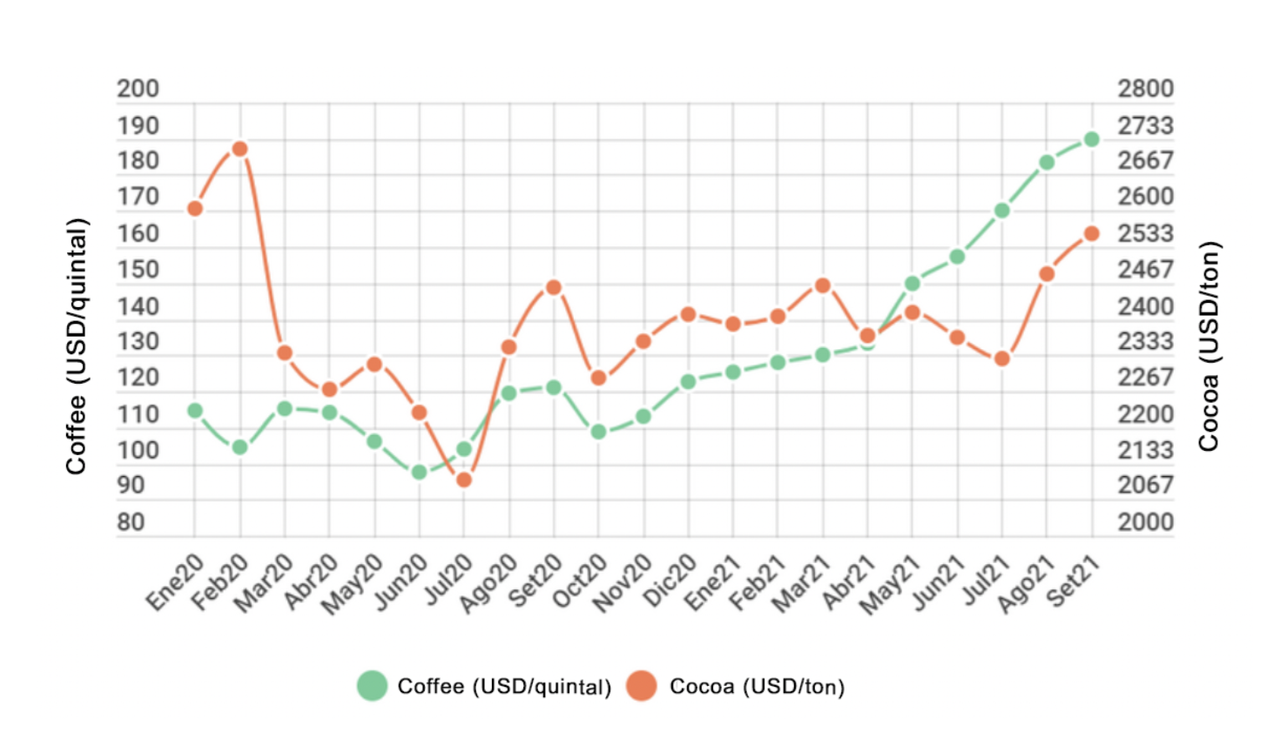

In the case of coffee, the positive trend in international prices has played a very important role in the economy of producer families, since they have mitigated the volatility of international markets, especially in the months of greatest restrictions worldwide.

In the case of cocoa, the price factor also represented a positive element for the economy of the producing families, since the average price of shipments abroad went from 2.5 thousand USD per ton in 2019 to almost 2.7 thousand USD per ton in 2020.

In both cases, price volatility is a factor to consider. As world production recovers and with it, previous inventory levels, prices may fall to previous levels or close to them.

Graph 3. Evolution of international coffee and cocoa prices

Source: Intercontinental Exchange (ICE)(coffee), International Cocoa Organization (ICCO) (cocoa). Note: Both refer to New York Stock Exchange indicative prices.

How does 2021 close in both sectors?

For the coffee sector, the perspective is that the recovery of export levels is the most viable scenario, especially since the world's largest coffee-consuming economies have already resumed the dynamics of their economic activities and have almost eliminated globally the most of the restrictions. This, added to the maintenance of international coffee prices on the rise, gives encouraging signs.

On the cocoa side, the outlook is also encouraging, especially due to the internal initiatives of the international cooperation agencies that promote the production and marketing of this crop in the country. Perhaps the only current setback is the average price of shipments (between January and August of this year) that have had a slight drop (2%) compared to last year (January and August, 2020); however, international prices are showing signs of recovery in the last two months (August and September).

Therefore, a year-end is expected with a view to the recovery of the dynamics of both the coffee and cocoa sectors in Peru.

Fact:

The Peruvian Chamber of Coffee and Cocoa, in coordination with the Swiss Cooperation and within the framework of the Alliance Project for Sustainable and Competitive Coffee, works on guidelines and promotion plans that include among its objectives the promotion of domestic coffee consumption, which In turn, it contributes to reducing the incidence of poverty in Peruvian coffee growers by having an increase in their income. In this sense, we will continue to produce articles and content in which the consumer can find out up close what the current coffee activity is like.